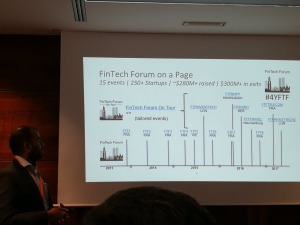

Announcing the line-up of startups for 9th FinTech Forum: 21st Sep. 2017

Check out the line-up of the startups selected so far to present at the 9th FinTech Forum on 21st Sep. 2017 in Frankfurt. The 4th anniversary edition since our inaugural event in Nov. 2013 kicks off with a scorecard of ca. 250 startups – indeed, also a reflection of the Continental Europe FinTech scene over the last four years.

Register here

ForgeRock raises $88 million in Series D round for further growth

Digital identity management firm ForgeRock has raised $88 million in a Series D round led by Accel with participation from KKR. First founded in Norway and now based in San Francisco, ForgeRock will invest the new funds in further development of the ForgeRock Identity Platform and plans to grow from 400 employees to 500 by the end of the year.

Read More…

Habito, an app that helps you find the right mortgage, raises £18.5M Series B led by Atomico

Habito, a London startup that is bringing the entire mortgage process online, has raised £18.5 million in Series B funding. Atomico, the European VC firm founded by Skype’s Niklas Zennström, led the round, with participation from existing investors Ribbit Capital, Mosaic Ventures, and Revolutionary (Ad)Ventures. It brings the total raised by the U.K. company to just over £27 million.

Read More…

Budget management app Linxo raised €20 million

Le Crédit Agricole et le Crédit Mutuel Arkéa réinvestissent dans la startup de la Fintech aixoise et la Maif entre au capital. C’est la plus grosse levée de fonds du secteur depuis deux ans.

Read More…

Online payment service Satispay raises €18 million

Satispay ha chiuso il terzo round di finanziamento. Con un target iniziale di 12 milioni di euro, l’aumento di capitale ha raggiunto la cifra record di 18,3 milioni, portando così la raccolta complessiva a 26,8 milioni, e ad una valutazione post money della società pari a circa 66 milioni.

Read More…

Seedrs raises another £4 million from Neil Woodford

Equity crowdfunding platform Seedrs has raised £4 million from Woodford Investment Management, the firm helmed by Neil Woodford.Woodford Investment Management previously invested £6 million in the startup, which now brings his total investment to £10 million.

Read More…

Accounting service sevDesk Offenburg gets €3.1 Million

LEA Partners und Wecken & Cie. investieren 3,1 Millionen in sevDesk. „Ausschlaggebend für unser Investment war insbesondere das Unternehmerduo hinter sevDesk, das uns sowohl fachlich als auch persönlich überzeugt hat“, sagt Sebastian Müller, Geschäftsführer von LEA Partners.

Read More…

Payment app Bam raises €1 million to save you money with cashback

Bam lève 1 million d’euros pour vous faire gagner de l’argent sur vos dépenses du quotidien

Read More…

Insurtech startup Neosurance raises €705,000 in seed funding

Neosurance, a Milan, Italy-based machine learning and AI-powered insurtech startup, raised €705K in seed funding.

Backers included strategic business angels, mainly managers and executives coming from the Italian and European insurance industry

Read More…

Money Dashboard Raises £1.33M in Equity Crowdfunding

Money Dashboard, an Edinburgh, UK-based personal finance management app, raised £1.33M in equity crowdfunding.

1708 investors have participated in the campaign via Crowdcube acquiring an equity stake of 9.55% in the company.

Read More…

Fintech startup Tink receives €1.4 million

Tinks låter sina användare betala räkningar, hålla koll på boräntan eller byta sparande från en bank till en annan via en app.Under det senaste året har Tink inlett samarbeten med olika banker och i början av 2016 tog bolaget in 85 Mkr från SEB och investmentbolaget Creades.

Read More…

FinTech startup Paybase gets £700,000 from Innovate UK

London-based FinTech startup Paybase has received a grant of almost £700,000 from innovation agency Innovate UK.

Read More…

Car insurance app Drivies raises €500,000

Drivies es una nueva startup que ha desarrollado una app que detecta automáticamente la forma de conducción y utiliza Inteligencia Artificial para ofrecer a los conductores un mejor precio en el seguro del coche y ventajas alrededor de la conducción.

Read More…

Fintech startup Bittiq raises seed round from newly launched Holland Startup Capital

Utrecht based startup Bittiq has raised an undisclosed seed round from the newly launched angel fund Holland Startup Capital I. Bittiq will use the capital raised to develop its mobile app. The public launch of the platform will follow by the end of the year, in anticipation of the European financial directive PSD2 in January 2018.

Read More…

Insurance broker invests in Insurtech Startup esurance.ch

Die ASSEPRO-Gruppe mit ihren Tochtergesellschaften Fraumünster Insurance Experts und swissbroke beteiligt sich an der stark wachsenden esurance.ch und investiert damit als erster grosser Schweizer Versicherungsbroker in ein InsurTech-Unternehmen.

Read More…

Fintech startup Capcito has raised €500,000

Nu berättar Capcitos medgrundare Michael Hansen att Peter Gyllenhammar gått in med ytterligare 2,5 miljoner kronor i bolaget, även denna gång genom sitt fastighetsbolag.

Read More…

CREALOGIX acquires AI technology of Koemei

CREALOGIX, a fintech company and market leader in digital banking, has purchased the artificial intelligence (AI) technology of Koemei, a spin-off of the IDIAP Research Institute based in Martigny, Wallis. Koemei’s solution enables for automated conversion of audio and video content into text data for analytics and optimisation, thanks to machine learning technology. CREALOGIX will adapt the technology as of autumn 2017.

Read More…

BNP Paribas buys majority stake in robo-advisor Gambit

BNP Paribas has made a move into the robo-advisory sector, buying a majority stake in Belgian specialist Gambit Financial Solutions. Terms of the deal were not disclosed.

Read More…

Atom Bank targets German retail savings market

British app-only bank Atom is making a move into the German market through partnership with local startup Deposit Solutions.

Read More…

Warum setzt Finleap jetzt auf ein Hacker-Startup?

Die Berliner Firmenfabrik Finleap, die Startups im Bereich Finanzen und Versicherungen gründet, hat ihr neues Venture vorgestellt. Das Unternehmen mit dem Namen Perseus plant, kleinen und mittelständischen Unternehmen Cybersicherheit zu bieten. Seit dem heutigen Montag läuft die Beta-Version des Services, an dem laut Süddeutscher Zeitung auch die Hannover Rück beteiligt ist.

Read More…

Deutsche Bank boss says ‚big number‘ will be replaced by robots

John Cryan, chief executive of Deutsche Bank, has told an audience of bankers in Frankfurt that he expects a „big number“ of his current staff to be replaced by robots

Read More…

UK fintech firms expect revenues to soar

Despite Brexit, the UK’s fintech firms remain bullish on their prospects, with half expecting revenues to double over the next 12 months and a third even anticipating an IPO within five years, according to a survey for Her Majesty’s Treasury.

Read More…

German digital insurance startup Coya receives $10 million from Silicon Valley

Berlin-based insurtech startup Coya has raised a $10 million seed funding round. the investment was led by Silicon Valley’s Valar Ventures, a VC firm backed by Peter Thiel, with participation from e.ventures and La Famiglia. Thiel, a co-founder of PayPal, is known for investing in European fintech startups, including the UK’s TransferWise and Germany’s N26.

Read More…

Danish payments processor Nets close to $5bn buyout

Nets, the largest payments processor in Scandinavia, is rumoured to be close to a private equity buy-out that would value the company at more than $5bn, according to a report from the Financial Times.

Read More…

Tilbago lanciert Robo-Inkasso

Nach Robo-Advisorn und Robo-Buchhaltung kommt nun das Robo-Inkasso. Lanciert wurde der Service diese Woche vom Luzerner Startup tilbago. Das Robo-Inkasso Robo-Inkasso überwacht den Fortschritt jeder einzelnen Betreibung ohne Zutun des Gläubigers und leitet bei Bedarf selbständig notwendige Aktivitäten ein.

Read More…

Etherisc verlegt Sitz ins Crypto Valley

Das auf den Aufbau einer dezentralisierten Versicherungsplattform spezialisierte Blockchain-Startup Etherisc geht mit dem Zuger Early-Stage-Investor Lakeside Partners und dem Beratungsunternehmen inacta eine enge Partnerschaft ein und verlegt den Hauptsitz von Deutschland ins Crypto Valley.

Read More…

Advanon wird in Deutschland aktiv

Seit Januar 2017 hat Advanon eine Zweigniederlassung in Berlin und ab August 2017 sind nun auch die Dienste des Schweizer Fintech Startups für deutsche KMU verfügbar. Das Startup bietet mit seiner Plattform, die Investoren und KMU verbindet, eine schnelle und einfache Factoring-Alternative.

Read More…

Kaffee mit Bitcoin bezahlen? Dieser Gründer will das leicht machen

Julian Hosp hat Großes vor: Er will Kryptowährungen alltagstauglich machen. Dazu rührt er ordentlich die Werbetrommel, schreibt Blogeinträge, spricht Podcasts und macht Youtube-Videos. Mit seinem Startup TenX hat er außerdem eine Krypto-Bankkarte entwickelt.

Read More…

taxbutler-Investment: Jens Spahn macht Rückzieher

Jens Spahn (CDU) will seine umstrittene Beteiligung an einem jungen Unternehmen der Fintech-Szene aufgeben” – berichtet die “Süddeutsche Zeitung”. In der vergangenen Woche wurde bekannt, dass Spahn 15.000 Euro in taxbutler investiert hat.

Read More…

Wirecard Offers Cashless End-to-end Solution for Europe’s Largest Taxi Booking App taxi.eu

Wirecard, the leading provider of payment and internet technology, will in future process all online payments for the taxi.eu app. The app is designed by fms/Austrosoft, a taxi fleet management system manufacturer, and is Europe’s largest taxi booking portal with more than 65,000 connected vehicles in over 100 European locations.

Read More…

IDnow gewinnt vor Gericht gegen Wettbewerber WebID

Schon vor einem halben Jahr stand IDnow vor Gericht – gegen einen mächtigen Gegner. Die Deutsche Post warf dem Startup damals vor, seine Werbung sei „irreführend und wettbewerbswidrig“. Das junge Unternehmen ließ es auf das Verfahren ankommen und siegte.

Read More…